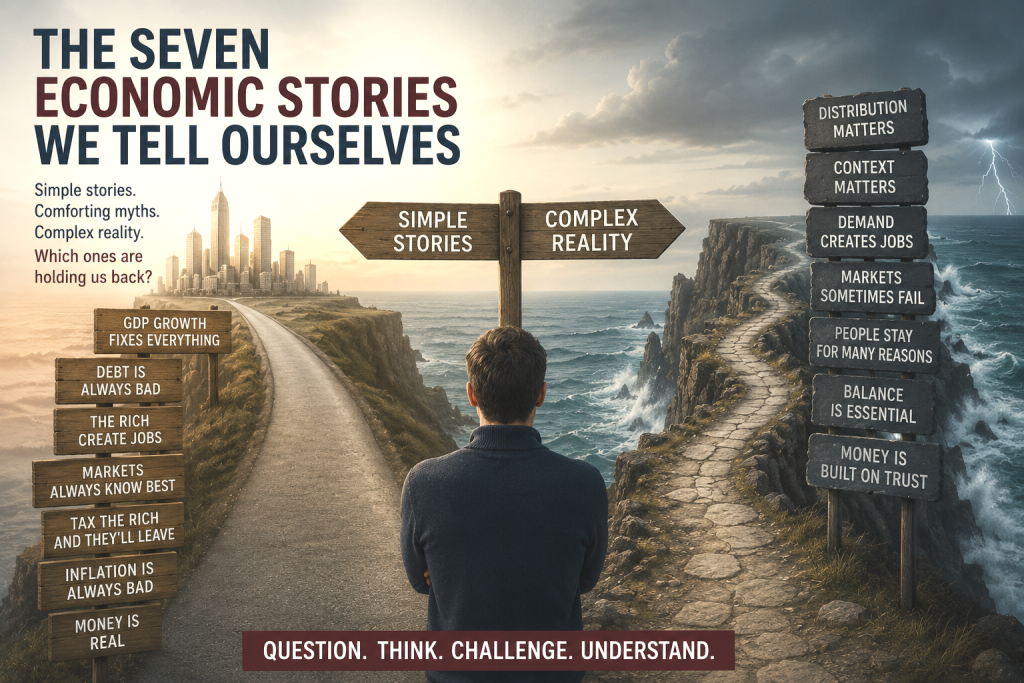

Last week I questioned whether our current school curriculum provides us with the knowledge we require for handling money during our adult life. This week I’d like to look at seven common economic myths I consequently grew up with that, I believe, should be examined by students in today’s education system.

Economics is often presented as a science of numbers. We hear about growth rates, inflation figures, government debt and stock market performance. Experts produce graphs. Politicians quote statistics. Journalists report percentages.

Yet much of our thinking about economics is not based on facts. We inherit economic beliefs in much the same way that we inherit religious beliefs, political loyalties, or assumptions about human nature. They become part of our mental furniture. We rarely examine them. We simply assume they are true.

Here are seven economic stories many of us have been taught to believe.

Myth No. 1. If GDP Is Growing, Everything Must Be Fine

One of the most common assumptions is that economic growth automatically means social progress. If the Gross Domestic Product is increasing, politicians congratulate themselves, commentators celebrate and newspapers announce that the economy is doing well.

But there is an obvious question that often goes unasked: doing well for whom?

GDP measures economic activity. It measures production. It tells us how much a country produces and sells. What it does not tell us is how that wealth is distributed or whether ordinary people are benefiting from it.

A nation can have impressive growth while housing becomes unaffordable, public services deteriorate and large sections of the population struggle to make ends meet.

As a former teacher, I sometimes compare GDP with examination results. A school may improve its statistics while becoming a worse place to learn. The numbers can look impressive while something essential is being lost.

The same is true of nations. Economic growth matters, but it is not the same thing as human flourishing.

Myth No. 2. Debt Is Always Bad

Most of us are taught to fear debt. For individuals, that is often sensible. Excessive borrowing can destroy lives. It can create stress, dependency and hardship. Yet not all debt is the same.

A mortgage, a student loan or a business investment is different from borrowing money to fund reckless consumption. One creates future value; the other merely brings tomorrow’s spending into today.

The same principle applies to governments. When a state borrows to invest in education, infrastructure, scientific research or healthcare, it may be creating assets that benefit future generations. The question is not whether debt exists, but whether the borrowing is productive and sustainable.

The most successful economies in the world often carry substantial public debt. What matters is not the existence of debt itself, but the wisdom with which it is used.

Myth No. 3. The Rich Create Jobs

This idea appears so frequently in political debate that many people accept it without question. There is, of course, some truth in it. Entrepreneurs create businesses. Businesses employ people. Investment can stimulate growth. But the story is incomplete.

Businesses do not hire employees simply because their owners are wealthy. They hire employees because there is demand for their products and services. A restaurant expands because customers fill its tables. A manufacturer recruits workers because orders are increasing. A shop hires staff because people are buying what it sells.

In other words, jobs are not created by wealth alone. They are created by economic activity. Moreover, much employment comes not from billionaires or multinational corporations, but from small and medium-sized businesses. Across Europe, countless family businesses, local shops, tradespeople and self-employed entrepreneurs collectively employ millions of people.

The real engine of employment is not wealth itself but a healthy and active economy.

Myth No. 4. Markets Always Know Best

For some people, the market has become almost a secular religion. The argument is familiar. Left alone, markets allocate resources efficiently. Government intervention merely creates distortions and stunts economic growth.

There is certainly some truth in this. Competitive markets can be remarkably effective. They often encourage innovation, efficiency and consumer choice. But markets are not infallible.

Consider healthcare. If access to medical treatment depends entirely upon ability to pay, many vulnerable people will be excluded.

Consider environmental protection. Businesses may profit by passing environmental costs onto society as a whole. Pollution becomes someone else’s problem.

Economists even have a term for these situations: market failures.

The reality is that markets and governments each have strengths and weaknesses. Mature societies require both. The challenge is not choosing one over the other, but finding the right balance between them.

Whenever someone insists that the answer is always more market or always more state, I become suspicious. Human societies are rarely that simple.

Myth No. 5. If You Tax the Rich, They Will Leave

This argument appears whenever tax reform is proposed. Raise taxes on wealthy individuals, we are told, and they will immediately pack their bags and move elsewhere.

At first glance, the claim seems plausible. Yet people are not spreadsheets.

Human beings make decisions based on family, friendships, culture, language, quality of life, security and belonging. Financial considerations matter, but they are rarely the only consideration.

Countries such as Norway, Sweden and Denmark have maintained relatively high levels of taxation while remaining prosperous, innovative and attractive places to live.

This does not mean taxes can be increased without limit. Excessive taxation can certainly discourage investment and entrepreneurship.

The point is simply that reality is more nuanced than political slogans suggest.

People stay for many reasons. They leave for many reasons. Tax is only one factor among many.

Myth No. 6. Inflation Is Always Bad

The word inflation usually arrives wrapped in anxiety. We hear that prices are rising and immediately assume disaster.

Certainly, high inflation can be deeply damaging. It erodes savings, creates uncertainty and hits those on lower incomes particularly hard. Yet economists generally do not aim for zero inflation.

A modest level of inflation is usually considered healthy because it reflects a growing economy. It encourages spending, investment and economic activity.

What is often forgotten is that the opposite problem can be equally dangerous.

If prices continually fall, people postpone purchases. Why buy today if everything will be cheaper tomorrow? Businesses then sell less, investment slows and unemployment may rise.

Like many things in life, the issue is not inflation versus no inflation. It is balance. Too much inflation can be destructive. Too little can be equally problematic.

Myth No. 7. Money Is Real

This final myth is my favourite because it takes us beyond economics and into philosophy.

Most of us think of money as something solid and tangible. We earn it, spend it, save it and worry about it. Yet money possesses no intrinsic value.

A fifty-euro note is merely paper. The number displayed in your bank account is simply a digital record stored on a computer somewhere.

Money works because we collectively believe it works. Its value depends upon trust.

This is not as strange as it sounds. Much of human civilisation rests upon shared beliefs. Nations exist because enough people believe they exist. Laws function because people collectively accept their legitimacy. Companies, universities and governments all depend upon systems of shared trust.

Money is one of humanity’s most successful collective stories. That does not make it imaginary. It makes it a social construct, like any other.

And perhaps that is one of the most important lessons economics can teach us.

If only I’d known in my twenties what I know now

If there is a lesson I wish somebody had taught me when I was starting out, it is that wealth is rarely built through cleverness alone. Looking back, the people who seem to achieve financial security are often not the most intelligent, the most educated or even the highest earners.

They are the people who consistently do a few simple things well.

-

- They spend less than they earn

- They avoid unnecessary debt

- They acquire productive assets

- They diversify their investment portfolio

- They think long term

- And above all, they allow time and compounding to work their quiet magic.

Perhaps that is the greatest economic lesson of all. Not that there are easy answers. But that small, sensible decisions repeated over decades are often more powerful than brilliant ideas pursued for a few months.

Beyond Economics

The purpose of examining these myths is not to replace one certainty with another.

It is to become more cautious whenever someone offers a simple explanation for a complicated problem.

Economic debates are often presented as battles between truth and error, between common sense and foolishness, between left and right. Reality is usually less satisfying.

The older I become, the less interested I am in certainty and the more interested I am in questions.

-

- Who benefits from economic growth?

- What kind of debt creates value?

- When do markets work well, and when do they fail?

- How much inequality can a society tolerate before trust begins to erode?

And perhaps most intriguingly of all: what other things do we collectively believe in that are no less dependent on faith than money itself?

Economics turns out to be about far more than money.

It is about human beings and the stories we tell ourselves about how society works.

The test of a first-rate intelligence is the ability to hold two opposed ideas in mind at the same time and still retain the ability to function.

— F. Scott Fitzgerald