Navid Kermani addressing Bundeswehr recruits at the Bendlerblock, Berlin, on 20 July 2026.

On 20 July, Germany held its annual public oath ceremony for new Bundeswehr recruits in Berlin. The date was no coincidence. It commemorates the failed assassination attempt on Adolf Hitler by Colonel Claus von Stauffenberg and a small group of German officers in 1944.

They failed. They were arrested, tortured and executed as traitors.

Today they are remembered as patriots.

This year’s keynote address was delivered by the distinguished German-Iranian writer Navid Kermani, one of Germany’s most respected public intellectuals and a recipient of the Peace Prize of the German Book Trade. His speeches are rarely designed to provoke outrage. This one did.

Referring to the recent military action by the United States and Israel against Iran, Kermani described the conflict as “manifestly contrary to international law and politically disastrous”. He then turned to the young men and women standing before him and said something remarkable. If a future German government were ever to lead them into such a war, he argued, it would be their duty to refuse the order.

I think they completely missed the point. Kermani was not really talking about Israel or Iran. He was asking one of the oldest and most uncomfortable questions in political philosophy: to whom does a soldier owe ultimate allegiance?

At first sight, the answer seems obvious. Soldiers are trained to obey orders. No army could function if every command became the subject of debate. Discipline, trust and obedience are indispensable to military life.

But history teaches us that obedience cannot be an absolute virtue. The twentieth century settled that argument at terrible cost.

When the Second World War ended, the judges at Nuremberg rejected the defence offered by so many of those standing before them: I was only following orders. From that moment onwards, the modern world accepted that individual human beings remain morally responsible for what they do, even when acting under orders.

Germany drew a profound lesson from that catastrophe. The Bundeswehr was deliberately founded on the principle of the citizen in uniform. A German soldier is expected not merely to fight well, but to think morally. Military service does not suspend personal responsibility; it demands it.

That principle has never been more relevant than it is today. Modern warfare increasingly takes place at a distance. A missile is launched hundreds of kilometres away. A drone circles silently above a city. A pilot receives coordinates on a screen. Somewhere below are buildings that military intelligence has identified as legitimate targets.

But intelligence is not infallible. Civilians are.

Schools, hospitals and residential apartment blocks have repeatedly become the scenes of devastating attacks in recent conflicts, whether in Gaza, Lebanon, Ukraine, Sudan or elsewhere. Governments justify them. Opponents condemn them. Lawyers spend years arguing over proportionality, military necessity and international humanitarian law.

None of that alters one simple fact: at some point, a human being still presses the button.

That is the moral burden Kermani placed before Germany’s newest soldiers. A question that one day may confront every man and woman who wears a military uniform.

Young Bundeswehr recruits taking their oath to serve the Federal Republic of Germany.

Of course, international law contains difficult cases. Kermani himself acknowledged that. Questions of pre-emptive self-defence, proportionality and military necessity are often disputed by serious lawyers acting in good faith. Yet he also made a distinction that deserves careful attention. Not every case is difficult.

There are actions so obviously incompatible with the principles of humanity that no legal textbook is required to recognise them. Deliberately targeting civilians. Destroying hospitals. Treating an entire civilian population as expendable. History has taught us, again and again, where such thinking leads.

This is why the anniversary of 20 July matters. The officers who conspired against Hitler broke their oath to the German government because they believed a higher loyalty had taken precedence. Their own state condemned them. History vindicated them. That is not a uniquely German lesson for it belongs to every democracy.

Patriotism does not consist of supporting every decision taken by one’s government. Governments are temporary. Political leaders come and go. Wars begin and end. The rule of law and the equal value of every human life are meant to endure.

That is why Kermani’s speech matters far beyond Germany. He reminded us that democracy ultimately depends upon citizens and soldiers who understand that conscience is not the enemy of duty but one of its foundations.

Without that conviction, “Never again” becomes little more than an annual slogan.

With it, those words retain their meaning.

“If a future German government should lead you into a war that is as clearly in violation of international law and as politically disastrous as the recent war waged by the United States and Israel against Iran, then it will be your duty to refuse that order.” — Navid Kermani

His argument is straightforward: government should judge its success not merely by economic growth, favourable statistics or the approval of financial markets, but by whether life genuinely improves for ordinary people in communities such as Makerfield and thousands of places like it.

What does a rising GDP mean to a family struggling to pay its bills?

What comfort is a buoyant stock market to someone unable to afford their first home?

For too long, British politics has often spoken as though national success could be measured from Westminster, the Treasury or the City of London. Burnham’s challenge is refreshingly different. He asks us to begin where people actually live.

It is a powerful idea, but it is also a deceptively difficult one.

Because the moment we move from slogans to governing, the Makerfield Test encounters questions for which there are no easy answers.

Beyond Makerfield

Imagine Britain needs to increase defence spending dramatically because the international situation has become more dangerous.

The additional money has to come from somewhere. Taxes rise. Public spending elsewhere is reduced.

Does the Makerfield Test say this is the wrong decision because local communities feel poorer?

Or does national security sometimes require short-term sacrifice?

Consider trade.

A new agreement with another country creates thousands of jobs nationwide but causes one manufacturing town to lose its largest employer.

Has the policy succeeded?

Or failed?

Or what about climate policy?

Higher carbon taxes may increase household costs today while helping avoid much greater environmental damage tomorrow.

Should governments refuse such policies because today’s voters bear the immediate pain?

Or should they ask communities to accept temporary hardship for future generations?

The same questions arise with infrastructure.

A high-speed rail line may transform one region while another loses investment and homes are demolished.

A new airport may create prosperity for hundreds of thousands while disrupting the lives of nearby residents.

Every major decision produces winners and losers.

The Makerfield Test asks us to judge policy locally.

But governments must also govern nationally, and of course internationally.

The immigration dilemma

Immigration presents perhaps the clearest example.

Economists frequently argue that immigration strengthens Britain’s economy over the long term by addressing labour shortages, increasing tax revenues and supporting an ageing population.

Yet those national benefits may be accompanied by genuine local pressures.

Schools become more crowded. GP appointments become harder to obtain. Housing demand increases. Communities experience rapid cultural change.

These concerns deserve neither dismissal nor exaggeration.

But they exist alongside equally real national needs.

Which perspective should prevail?

Should government prioritise the immediate experience of individual communities?

Or the country’s long-term economic and demographic interests?

The Makerfield Test offers an important moral instinct, but it doesn’t automatically provide an answer.

The burden of hope

There is another challenge.

Political hope can be a dangerous thing because expectations have a habit of outrunning reality.

Following Burnham’s emergence on the national stage, several commentators observed that his rhetoric was generating extraordinary optimism. Communities neglected for decades understandably wanted to believe that someone had finally recognised their experience.

Yet history offers a warning. The higher the expectations, the greater the disappointment when government inevitably encounters limits.

This is not unique to Burnham. It happened to Tony Blair, Barack Obama and Emmanuel Macron.

Democratic politics has a recurring pattern: campaigns promise transformation > Government discovers constraint > Voters experience frustration > The cycle begins again.

If Burnham persuades people that every decision will pass the Makerfield Test, he has also created a standard against which every decision will be judged.

That is both politically courageous and politically risky.

Judging the government by its own standard

This is where the Makerfield Test becomes genuinely useful.

If governments ask to be judged by the lives of ordinary people, then ordinary people are entitled to ask difficult questions.

Why was this policy chosen?

Why this priority rather than another?

Who benefits first?

Who waits?

Who pays?

Who gains?

These are very reasonable democratic questions.

Indeed, they are precisely the questions the Makerfield Test encourages us to ask.

The standard should apply not only to previous governments but also to those who introduce it.

The unavoidable dilemma

Ultimately, every government confronts the same uncomfortable reality.

Resources are finite.

Competing priorities are unavoidable.

Perfect fairness is impossible.

Sooner or later, ministers must decide that one place receives investment before another.

One project proceeds while another is delayed.

One industry expands while another declines.

One generation bears costs that another generation may eventually enjoy.

No political philosophy can eliminate these choices.

It can only explain how they should be made.

That is why I find the Makerfield Test both so compelling and so incomplete.

It reminds us that statistics are not people and that national prosperity means little if communities experience only decline.

But governing Britain also requires another perspective.

Sometimes a difficult national decision genuinely serves the country’s long-term interests, even when particular communities understandably object.

Sometimes today’s sacrifice becomes tomorrow’s prosperity.

Sometimes it doesn’t.

The difficulty lies in knowing the difference.

The real test

The most important question raised by the Makerfield Test is:

Who decides when Makerfield should lose for Britain’s long-term benefit?

That question has no comfortable answer.

Every government, whatever its political colour, will eventually ask one town, one industry, one region or one generation to accept sacrifice for a wider national goal.

The challenge is not avoiding those moments.

The challenge is ensuring they are honest, proportionate, accountable and genuinely necessary. And, better still, that they line up with a clear vision and values for which politicians have been elected.

“Parliament is not a congress of ambassadors from different and hostile interests… but a deliberative assembly of one nation, with one interest, that of the whole.” — Edmund Burke

I have come to realise that the most valuable education I ever received was learning to see the same country from two completely different points of view.

I was reminded of this recently while listening to Andy Burnham speak about the “Makerfield test”: his promise that national policy should be judged by whether it improves life in places such as Makerfield, rather than merely satisfying the economic and political orthodoxies of Westminster.

I was attracted to the idea immediately. That was not altogether surprising. Burnham and I have several things in common.

We both came from relatively humble backgrounds in the North of England. We both went on to study humanities at Oxbridge — English at Cambridge in his case, French and German at Oxford in mine. We both entered worlds far removed from those in which we had grown up. And both of us, in very different ways and on vastly different public stages, appear to have become increasingly interested in the distance between the Britain described by its institutions and the Britain experienced by many of its people.

That does not mean I agree with Burnham on every issue. I don’t.

What interests me is the journey between two social worlds, and what that journey allows a person to see.

Learning to see two Britains

Social mobility is normally described as movement in one direction.

A child from an ordinary background works hard, receives a good education, enters a prestigious university and rises into a more prosperous or influential part of society. The story is presented as an escape: departure from one world and successful arrival in another.

But that is not quite how it feels. You do not necessarily leave the first world behind. Instead, you acquire a second vantage point.

At Oxford, I encountered people whose intelligence and talent were undeniable. But I also encountered people who had been prepared from childhood to enter rooms in which power was exercised. They understood the vocabulary, the conventions and the unwritten rules. They spoke to professors, employers and authority figures with an assurance that did not always reflect greater ability. It often reflected something simpler: nobody had ever suggested to them that the room might not belong to them.

This is one of the least discussed advantages of privilege.

Privilege does not always announce itself as wealth. Sometimes it appears as confidence. It appears as ease in unfamiliar surroundings, freedom from embarrassment, fluency in the language of institutions and the assumption that one’s opinions will be heard.

To the person who possesses these advantages, they may feel like competence.

To the person who does not, the absence of them may feel like personal failure.

Crossing the class divide teaches you to recognise the difference.

You remember the families for whom an unexpected bill is not an inconvenience, but a crisis. You remember people who are intelligent but have never been encouraged to think of universities, professions or public life as places for them. You remember how authority looks from below.

But you also begin to understand the people who design policies, manage institutions, allocate capital and shape public debate. You learn their language. Sometimes you become one of them.

You see Britain from both sides.

What economic success looks like from below

This double vision changes the meaning of economic statistics.

A government announces that the economy is growing. The stock market rises. Corporate profits increase. Property becomes more valuable. Ministers point to employment figures and national averages as evidence that the country is succeeding.

All of these measurements may be accurate.

But they do not answer the most important question:

Who is experiencing the success?

A rise in property prices is good news for someone who owns several properties. It may be disastrous for somebody trying to buy a first home.

A strong stock market enriches people with substantial investments and pensions. It means far less to families who own no financial assets and are struggling to pay their electricity bills.

Seen from Westminster, these may appear to be complications within an otherwise successful economic model.

Seen from Makerfield, or from many towns across northern England such as Runcorn where I grew up, they may be the model’s most important result.

This is why Burnham’s test has such immediate emotional force. It asks politicians to stop treating people as supporting evidence for an economic theory and instead ask whether the theory is improving their lives.

But it also reflects a more general truth: your assessment of any system depends partly on where you are standing inside it.

The education hidden inside the humanities

There may be another reason Burnham and I are drawn towards this way of thinking.

Neither of us studied economics, management, law or PPE. We studied humanities.

In modern public debate, the humanities are often treated as decorative. Science, technology and economics are described as useful, while literature, languages, history and philosophy are expected to justify their existence.

But the humanities teach something our political and economic systems desperately need.

They teach us to enter realities other than our own.

A novel asks us to inhabit another person’s consciousness. History asks how people and societies arrived at their present condition. Philosophy asks what we owe one another. A foreign language teaches that our own way of dividing, naming and expressing reality is not the only possible one.

Studying French and German did more than enable me to communicate in other languages. It challenged the unconscious assumption that the British way of seeing the world was the natural or neutral one.

Living abroad later deepened that lesson.

After 16 years in Germany, and now beginning a new life in Spain with an Indonesian husband, I no longer see Britain entirely from within Britain. Europe is not an abstract bureaucracy called “Brussels”. Migration is not simply a number in a newspaper. Borders, residence rights and administrative systems are no longer theoretical matters. Foreign policy is no longer conducted in distant countries inhabited by anonymous populations.

To live between countries is to acquire another form of double vision. You become what I term “an accidental outsider.”

You see your own nation more clearly because you are no longer surrounded by its assumptions, something I had experienced at an abstract level in the writings of Diderot and Voltaire.

You also become more suspicious of political systems that can calculate the economic cost of a decision while remaining curiously unable to imagine its human consequences.

Data can tell us where poverty exists.

Literature may help us understand what poverty does to a person.

Economics can measure migration.

Languages and lived experience may help us understand what it means to become a migrant.

Statistics can tell us that a region is declining.

History can explain why its people no longer trust the institutions announcing the latest programme for their renewal.

The humanities are not a retreat from the real world. They are among our best defences against governing that world without sufficiently understanding the people who live in it.

Britain’s geography of power

The same question of perspective applies to the way Britain is governed.

The United Kingdom remains extraordinarily centralised. Regions with distinct histories, economies and identities are repeatedly expected to apply for funding, permission or attention from London.

The underlying assumption is rarely questioned: wisdom and legitimacy become more concentrated as one moves closer to Whitehall.

Burnham’s political experience in Greater Manchester has led him towards a different conclusion. His argument for greater devolution is not merely that Westminster sometimes makes the wrong decisions. It is that Westminster makes too many decisions in the first place.

This matters because the centre inevitably sees places differently from the people who live there.

From London, a town may appear as a collection of indicators: productivity, employment, educational attainment, transport connectivity and levels of deprivation.

From inside that town, it is a network of memory, identity, family, opportunity and loss.

Policies designed remotely may be rational in aggregate and destructive in practice. They may improve a national average while hollowing out a particular community. They may create efficiencies that look impressive in a report and feel like abandonment on the ground.

Perhaps Britain’s problem is not simply that Westminster has forgotten the North.

Perhaps the deeper problem is that Westminster still believes it has the right to remember the North on the North’s behalf.

Social mobility is not enough

For decades, Britain has presented social mobility as the answer to inequality.

Find talented children from modest backgrounds. Help them reach excellent universities. Allow them to enter professions and institutions previously closed to them.

That is worthwhile. My own life was transformed by educational opportunity.

But there is an uncomfortable limitation to this model.

Social mobility can help individuals escape an unequal system without making the system itself more equal.

A society cannot solve regional poverty by helping a small number of successful young people leave poorer regions. Nor can it solve class inequality simply by allowing exceptional individuals to join an existing elite.

The question is not only how many people can climb the ladder.

We must also ask who built the ladder, where it leads, and why so many people are expected to remain beneath it.

The greatest social value of mobility may therefore lie not in personal advancement but in the perspective carried across the divide.

Institutions need people who know what those institutions look like from outside.

Universities need people who remember what it felt like to believe university was “not for people like us”.

Governments need people who understand that a policy can be statistically successful and humanly disastrous.

The media need people who recognise that the national conversation is often conducted in a language millions of citizens neither use nor trust.

And prosperous societies need people who understand that poverty is not merely the absence of money. It is often the absence of margin, choice, confidence and the expectation of being heard.

The responsibility of seeing both sides

There is, however, no automatic virtue in crossing a social boundary.

People can enter privileged institutions and adopt their assumptions completely. They can use education to distance themselves from their origins. They can become more contemptuous of those who did not make the same journey, imagining that personal success proves the system is fair.

Indeed, meritocracy can create a particularly unforgiving elite.

If successful people believe they reached the top entirely through talent and effort, they may conclude that everybody who remained below simply failed to try hard enough.

Double vision, or becoming an accidental outsider, must therefore be preserved deliberately. It requires memory. It requires humility.

It requires an awareness that intelligence is widely distributed even when opportunity is not.

It also requires resisting the comforting idea that entering a powerful institution means fully understanding the people over whom that institution exercises power.

This may be the most valuable thing a person from a modest background can carry into an elite room: not authenticity as a performance, nor a sentimental claim to represent everyone they grew up alongside, but the knowledge that the world looks radically different depending on which side of the door you occupy.

The most important education

Oxford changed my life.

It gave me knowledge, confidence and opportunities my younger self could scarcely have imagined. It introduced me to languages, cultures and ways of thinking that eventually carried me far beyond the country in which I was born.

But Oxford was only one part of my education.

The North taught me how power looks from a distance.

Oxford taught me how power explains itself.

Teaching showed me how institutions affect individual lives.

Living abroad taught me to see Britain from the outside.

And moving between these worlds taught me that no single vantage point is sufficient.

This is what I recognised in Burnham’s Makerfield test: not a complete political philosophy, and certainly not an answer to every difficult national and international question, but an insistence that perspective matters.

Who is speaking?

Where are they standing?

What can they see from there?

And what remains invisible to them?

We spend a great deal of time asking how to help more people cross Britain’s class divide.

Perhaps we should ask an additional question: how do we ensure that those who cross it employ their experience to create a fairer society?

“I thought about the breaks that had scored the rhythm of my life. Expansion through rupture. Where others built continuity, I built awareness. And though that awareness didn’t make me happy, it had made me lucid. These breaks had been my real education — violent scholarships in the art of seeing.” — Níco Durón, Teacher, there are things that I don’t want to learn.

Photo taken with Oppo X9 on 7th July 2026 at 06:37 am, f2, 15 mm.

“The heavens declare the glory of God.”

For almost ten years, belief in God shaped the way I looked at the night sky.

This morning, at six o’clock, I realised how completely that has changed.

I began my usual jog while Torremolinos was still asleep. The promenade along La Carihuela was almost empty. The only sounds were the rhythmic slap of my trainers against the pavement and the gentle breathing of the Mediterranean.

I reached the harbour wall at Benalmádena just before sunrise.

The sea looked like polished, rippled glass.

Above me, Venus still shone brightly in the deep blue sky while the first orange light slowly crept over the mountains of the Sierra Nevada. They didn’t merely look beautiful. Those mountains are themselves the product of millions of years of continental collision, uplift and erosion. Even the backdrop to an ordinary sunrise carries an almost unimaginable history.

I sat. I started my meditation. I breathed. Then I opened my eyes and watched.

As the Sun finally appeared above the horizon, I found myself overwhelmed — not with worship, but with wonder.

Not because I imagined someone had painted the sunrise for me.

But because I knew what I was actually looking at.

He reminds us that reality is almost always far more astonishing than fiction.

Here are six examples.

1. You are travelling faster than a bullet…

…while sitting perfectly still.

The Earth rotates at about 1,670 km/h at the equator.

It orbits the Sun at roughly 107,000 km/h.

Our Solar System orbits the centre of the Milky Way at about 828,000 km/h.

Meanwhile, the Milky Way itself is hurtling through space at over two million kilometres per hour relative to the cosmic microwave background.

Right now, we are moving through the universe at extraordinary speed. We simply don’t notice because everything around us is travelling with us.

2. There are ten billion times more planets than hours since the Big Bang

Astronomers now estimate that our Milky Way alone contains around 100–400 billion stars, with most stars likely possessing planets.

Across the observable universe there may be around 10²⁴ planets.

That is one septillion planets.

If every second since the beginning of the universe represented one planet, you would still not have counted even a microscopic fraction of them.

3. Every atom inside your body is older than the Earth

The iron in our blood, the calcium in our bones, the oxygen we are breathing were all forged inside ancient stars that exploded billions of years before the Sun even existed. We are literally made of stardust.

Carl Sagan famously summarised it beautifully:

“We are a way for the cosmos to know itself.”

Literally.

4. The Mycoplasma cell

One of the smallest living things on Earth is a bacterium called Mycoplasma.

Around 5,000 of them placed end to end would stretch only one millimetre.

Yet inside that microscopic cell is a membrane, half a million DNA letters, hundreds of genes, molecular factories called ribosomes, and thousands of proteins performing countless chemical reactions every second.

It isn’t a blob. It is a self-maintaining chemical factory. And it’s alive.

That is magnificent.

5. There are more microbes living inside you than people who have ever lived

The average human body contains roughly 38 trillion bacteria, most living in the gut.

Without them, we couldn’t digest food, produce certain vitamins or even maintain a healthy immune system.

We are not one organism.

We are an ecosystem.

6. Everything alive is literally related.

A blue whale…

an oak tree…

a hummingbird…

a mushroom…

an octopus…

the bacteria living inside your intestine…

and you…

all use essentially the same genetic code.

Every living thing on Earth is related.

Not poetically, metaphorically or mythically.

Literally.

7. Tonight, when we look at the stars…

…we are looking into history.

The light from the Moon is about 1.3 seconds old.

From the Sun? Eight minutes.

From the nearest large galaxy, Andromeda? About 2.5 million years.

The light entering our eyes tonight began its journey when our ancestors were making stone tools.

The James Webb Space Telescope now observes galaxies whose light has travelled for more than 13 billion years.

We do not merely look across space.

We look backwards through time.

I honestly struggle to imagine anything more astonishing than that.

Then I remembered another way of seeing all this

There was a period of my life when I believed something very different.

For nearly ten years I was an evangelical Christian. I believed that God had created the heavens and the earth by speaking.

Genesis begins:

“And God said, ‘Let there be light,’ and there was light.”

— Genesis 1:3 (NIV)

I was taught that the universe ultimately existed to reveal God’s glory.

That human beings had been created to worship Him.

That no sunset, no mountain and no star could ever truly satisfy unless it led us to thank its Creator.

One argument particularly stayed with me.

What is the point of experiencing something beautiful, if you have nobody to thank for it?

At the time, that sounded deeply persuasive. Today, it doesn’t.

Wonder no longer needs an author

Ironically, losing my belief in God did not make the universe smaller.

It made it unimaginably larger.

Instead of being told the answers, I discovered questions.

Instead of certainty, I found endless curiosity.

Instead of myth, I found history.

Every mountain. Every whale. Every oak tree. Every coral reef. Every human brain. Every galaxy. Every living cell.

Each became vastly more interesting once I understood that none of them appeared fully formed.

Each carries within it an astonishing history stretching back billions of years.

Yet one certainty remains: we are constellations of atoms, stardust reassembled by chance and time, hurtling around our sun on a rock at 67,000 mph. DNA coils like ancient runes in every cell, issuing silent instructions: become, live, persist. From this choreography comes breath, thought, memory: a mother’s laughter, longing for distant places, a lover’s hand in the dark. We invent gods and heroes, build cathedrals and poems, grieve, and love. All this from fragile molecules wrapped in skin. Just chemistry. An echo of evolution.

And yet: is it not a miracle that matter dreams at all?

Today, I no longer see humanity as separate from nature. I know that the cells in my own body, the bacteria in my intestine, the dolphins swimming off this coastline, the pine trees on the Sierra Nevada and the swallows flying overhead are all distant cousins on one immense family tree stretching back nearly four billion years. Human unity is not simply a moral aspiration. It is a biological fact. So too is our kinship with every other living thing on Earth.

Does meaning require a creator?

I no longer think so.

Watching today’s sunrise did not feel empty because I wasn’t thanking somebody.

Quite the opposite.

It filled me with gratitude.

Not gratitude directed upwards.

But gratitude simply for existing at all.

For having evolved into a creature capable of understanding even a tiny fragment of what the universe is.

That is more than enough for me.

One unintended consequence

There is one further implication that I hadn’t appreciated when I was a Christian.

Some believers sincerely conclude that because God will one day replace this present world with “a new heaven and a new earth” (Revelation 21:1), environmental destruction is ultimately temporary.

Many Christians reject that conclusion and instead argue that humanity has a God-given responsibility to care for creation. I respect that view.

But I have encountered the first attitude often enough to think it matters.

Once this world becomes merely a waiting room for the next, its long-term future can begin to feel less urgent.

My own perspective has moved in the opposite direction.

If this is the only Earth our civilisation will ever inhabit, then every forest matters. Every coral reef matters. Every species matters.

Because this extraordinary planet is not a rehearsal.

It is home. Not just for human beings, but for every sentient fish, every majestic bird, every minuscule Mycoplasma.

Which story leaves you more awestruck?

One story says:

“And God said, ‘Let there be light.'”

The other says:

Hydrogen formed shortly after the Big Bang.

Gravity slowly gathered it into stars.

Those stars forged heavier elements.

Some exploded as supernovae.

Those atoms became planets.

One of those planets developed self-replicating chemistry.

After nearly four billion years of evolution, one species evolved capable of asking where it came from.

I know which story leaves me speechless.

Not because it is comforting.

But because it is true.

“The most beautiful experience we can have is the mysterious. It is the fundamental emotion that stands at the cradle of true art and true science.” — Albert Einstein

How the moon led me to rethink the origins of the universe and humanity’s place and responsibility within it.

As I settle into my new life in Spain, I wake up before dawn in order to jog along the promenade before it gets too hot, watch the sunrise, contemplate cosmology and meditate.

Last week, to the west above the Carihuela, there was a huge, bright, full moon poised low in the sky before the sunrise.

It wasn’t merely bright. It seemed suspended. As if detached from its control of the tides below. Silver against an increasingly blue sky, refusing — for a few precious minutes — to surrender to the approaching sun.

The sea below was calm. The seagulls were swooping down majestically to collect their breakfast. Somewhere behind me, the town was waking. Yet for a brief moment everything felt strangely timeless.

I stood there on the harbour wall longer than I intended. Not because I understood what I was looking at. Indeed, as I meditated, I was startled by how little I did.

That quiet moment began another of my recent intellectual odysseys. I jogged home and began researching in detail the origins of the universe.

The answers I discovered have profoundly changed the way I see both the universe and humanity.

We began with almost nothing

According to our best scientific understanding, the Universe began around 13.8 billion years ago.

In the first few minutes after the Big Bang, almost all that existed were the simplest elements imaginable: hydrogen, helium and tiny traces of lithium.

There was no carbon.

No oxygen.

No calcium.

No iron.

No chlorine.

No lead.

Nothing from which planets, oceans or living organisms could eventually be built.

Everything else had yet to be created.

Stars are not simply lights

The next discovery astonished me even more.

I had always thought of stars as glowing balls of gas.

In reality, they are unimaginably powerful nuclear furnaces.

The identity of every chemical element is determined simply by the number of protons in the nucleus of each atom.

Hydrogen has one proton.

Helium has two.

Carbon has six.

Oxygen has eight.

Iron has twenty-six.

Lead has eighty-two.

Inside stars, gravity compresses matter with such extraordinary force that atomic nuclei are pushed together in a process known as nuclear fusion.

When four hydrogen nuclei fuse together, they produce helium and release enormous amounts of energy.

Later, when stars become even hotter, three helium nuclei combine to create carbon. Carbon can then fuse with helium to produce oxygen. Larger stars continue building heavier and heavier elements through countless further fusion reactions.

Quite literally, the periodic table is assembled one proton at a time.

Eventually, the largest stars manufacture elements all the way to iron. When those stars finally exhaust their fuel, they explode as supernovae, scattering their newly created elements across the galaxy.

During those unimaginably violent explosions, still heavier elements such as gold, lead and uranium are created before being hurled into interstellar space.

Without generations of stars living and dying long before our Solar System existed, neither the Earth nor we ourselves could ever have existed.

For years I assumed that was simply a poetic metaphor.

It isn’t.

The hydrogen in the water within my body was formed shortly after the Big Bang itself.

But almost every other element within me has a different origin.

The carbon in my muscles.

The oxygen I breathe.

The calcium in my bones.

The iron carried around my body by my blood.

All of them were forged inside stars that died billions of years before the Earth even formed.

Some of those atoms may once have been part of ancient forests.

Some may have passed through dinosaurs.

Some may have circulated through countless generations of my own ancestors.

Matter itself is endlessly recycled.

The atoms change partners.

The universe never stops reusing its building blocks.

In this way, it is no coincidence that the branching networks of our neurons and the elegant spirals in hurricanes and elements of our DNA echo patterns that also appear throughout the cosmos. Different processes, different scales, yet strikingly familiar forms emerging from the same universe.

Then came another surprise

Just when I thought the story could not become any more remarkable, genetics added another layer.

Every person alive today shares common ancestry.

Research suggests that all living humans inherited their mitochondrial DNA from one woman who lived in Africa roughly 150,000 to 200,000 years ago.

Likewise, all living men inherited their Y chromosome from one man who lived much later.

They were not the only people alive at the time.

They are simply the individuals whose particular genetic lines survived uninterrupted to the present day.

Meanwhile, every generation doubles the number of our ancestors.

Travel back only a few thousand years and our family trees overlap so extensively that the distinctions between “my ancestors” and “your ancestors” begin to disappear.

In a very real biological sense, humanity is one enormous extended family.

A different foundation for responsibility

As the moon faded into the brightening Andalusian sky, I found myself asking a question that science itself cannot answer.

If Carl Sagan was right that “we are a way for the cosmos to know itself,” what follows logically from that?

As far as we currently know, nowhere else has the universe organised itself into beings capable of wondering where the universe came from.

Perhaps intelligent life is common throughout the cosmos.

I hope it is.

But until we know otherwise, we must take seriously the possibility that conscious beings like ourselves are extraordinarily rare. Maybe even unique.

If that is true, then our responsibility extends far beyond ourselves.

Protecting our planet.

Seeking truth.

Advancing knowledge.

Caring for one another.

Safeguarding future generations.

These are not merely useful social conventions.

They become responsibilities entrusted to the very few beings — perhaps the only beings — capable of understanding what is at stake.

The moon itself had not changed that morning.

Nor had the sea.

Nor the rising sun.

What changed was my understanding.

For the first time, I began to see humanity not as something standing apart from the universe, but as one of the most extraordinary things the universe has so far produced.

Perhaps, after all, the starry heavens above us do not merely invite our curiosity. They really can provide us with the most rational basis for human ethics that we will ever discover.

“Two things fill the mind with ever new and increasing admiration and awe… the starry heavens above me and the moral law within me.” — Immanuel Kant

How a Spanish football shirt unexpectedly changed the way I think about history, education and the origins of our globalised world.

I recently bought a Spanish football shirt to wear at a bar while watching Spain’s 3:0 win against Austria on Thursday.

That simple purchase unexpectedly led me down one of the most fascinating rabbit holes I have explored in a while.

It began with two Latin words embroidered on Spain’s coat of arms: Plus Ultra.

I knew from my school-Latin what the words meant, further beyond, but I still needed some context to understand the meaning.

A little research revealed that they are a reference to the Pillars of Hercules at the Strait of Gibraltar. For the ancient world, these marked the edge of the known earth. The old warning was “Non Plus Ultra” — nothing lies beyond.

Then came the voyages of exploration.

The warning became an invitation.

There was indeed more beyond.

That discovery prompted another question.

Christopher Columbus sailed for Spain. Yet I vaguely remembered reading somewhere that he was Italian. Was that right?

It was. I kept digging.

Born in Genoa, Columbus spent years trying to persuade different European rulers to finance his ambitious plan to reach Asia by sailing west. It was only when the Spanish Crown agreed to back him that history changed forever.

Then I discovered something even more surprising.

Ferdinand Magellan, whose expedition first circumnavigated the globe, wasn’t Spanish either. He was Portuguese. And he himself was killed in the Philippines before the expedition was completed.

Like Columbus, he simply happened to be sailing under the Spanish flag.

As I kept digging, I also learnt for the first time why America is called America and why the Pacific is called the Pacific. I learnt why Brazil speaks Portuguese while much of South America speaks Spanish, why Spain became one of history’s great global powers, how its sudden enormous wealth became a resource curse, and, most strikingly of all, how all these historical facts are mirrored in the events happening in the world today.

By now, all this led to another kind of question:

Why was I only learning this as I approach retirement?

None of these are obscure historical curiosities.

They explain the world we live in.

The more I thought about it, the more I realised that perhaps history has often been taught backwards.

Schools understandably devote considerable attention to national history. In Britain, we studied the Tudors, the Industrial Revolution and the Second World War. In Germany, where I spent many years teaching, National Socialism understandably occupies a central place throughout secondary education.

These are all profoundly important topics.

But too often history becomes an exercise in remembering names, dates, battles and treaties.

The examination rewards recall.

Real understanding often comes later.

History is not simply the story of what happened.

History can be the highly relevant explanation of why today’s world looks the way it does.

Why does almost an entire continent speak Spanish?

Why is Brazil different?

Why was Córdoba (Spain) once much bigger and more important than London?

Why are Europe and Latin America still so culturally intertwined?

Why and how did globalisation begin centuries before the Internet?

Those are historical questions too.

They just happen to illuminate the present rather than merely describe the past.

While I was training teachers at the University of Sussex, one of the finest history lessons I have ever witnessed contained almost no conventional history.

The young trainee teacher warned parents in advance that the lesson would be unusual.

She darkened the classroom. She played the sound of air-raid sirens followed by distant explosions. Beforehand, she asked the children to climb underneath their desks and lie silently on the floor with their eyes closed.

For several minutes they simply listened.

Afterwards she asked them to write, not about dates, military strategy or political leaders, but about how they had felt.

For a brief moment, those children had experienced uncertainty, vulnerability and fear. Not the reality of war, of course, but enough to begin imagining what it might feel like to be a child living through one.

I have forgotten countless historical dates since leaving school. I have never forgotten that lesson.

Nor, I suspect, have the children who experienced it.

That teacher wasn’t merely teaching history.

She was teaching empathy and vividly demonstrating how history is so relevant to life in the 21st Century.

As I have grown older, I find myself increasingly drawn to education that asks questions rather than rewards memorisation.

The same thought has appeared repeatedly in my recent writing about economics.

It is about understanding why economies behave as they do.

Likewise, history should not simply teach us to remember what happened.

It should help us understand why our world became what it is.

Perhaps that is why I have found these discoveries in Spain so unexpectedly exciting.

I wasn’t simply learning historical facts.

I was discovering connections.

The voyages of Columbus and Magellan were not isolated adventures.

They marked the beginning of the first great wave of globalisation.

Trade routes expanded.

Ideas travelled.

Plants, animals, diseases and cultures crossed oceans.

The Mediterranean outside my window here was once dry land – another fact I was unaware of. It is only thanks to the Zanclean Flood that water entered from the Atlantic through the Strait of Gibraltar and opened up the possibility of a future global trade highway.

The world became permanently interconnected.

Five centuries later we are still living with the consequences.

History also reminds us that no civilisation remains permanently at the top.

Sometimes I wonder whether schools unintentionally leave us with the impression that education ends when we pass our examinations.

In reality, the opposite is true.

The most rewarding learning often begins afterwards.

It begins when curiosity replaces obligation.

When we are no longer asking, “Will this be in the exam?”

Instead we ask, “Why did nobody ever explain this?”

A newspaper headline over breakfast in Spain made me question something I’d never really considered before. When a country’s economy is booming, who actually owns the wealth that’s being created?

One of the unexpected pleasures of moving to Spain has been rediscovering the lost art of breakfast.

Most mornings I walk to my favourite café, order a café con leche and toasted bread rubbed with fresh tomato and olive oil, then spend half an hour simply watching the town wake up. The same waiter greets familiar faces with effortless warmth. Elderly couples linger over coffee. Shopkeepers raise their shutters. Sunburnt tourists wobble by. There is something reassuring about the rhythm of ordinary life here.

A few mornings ago, however, it wasn’t the people who caught my attention. It was a newspaper.

The gentleman at the next table was reading Expansión, Spain’s financial newspaper. Across the front page was a headline that immediately made me stop.

Like most people, I have spent much of my life assuming that when a country’s economy grows, its people become wealthier. I’ve lived in Germany for 16 years, which always provided me with the perfect example.

And that is how the news is usually presented.

The economy is booming.

Corporate profits are rising.

The stock market reaches another record.

We instinctively hear those as different ways of saying the same thing.

But they are not.

Companies create wealth where they operate.

Ownership determines where much of that wealth ultimately accumulates.

The second receives part of the return from that prosperity.

Sometimes, of course, they are the same person.

Often they are not.

That morning, as I watched the waiter carrying coffees from table to table, it occurred to me that he was helping to create Spain’s prosperity every bit as much as a hotel owner, a banker or a company director. Every tourist welcomed, every breakfast served and every day’s work honestly completed contributes, however modestly, to a nation’s success.

Yet if one of Spain’s largest companies doubles its profits this year, a significant share of those profits may eventually belong to people who have never set foot in Spain.

The wealth is created here.

The ownership may be somewhere else.

For some reason, that simple distinction had never really occurred to me before.

A Global Story

The more I reflected on it, the more I realised that Spain was merely the setting.

This is the story of the modern world.

Capital crosses borders far more easily than people do.

That freedom has transformed our lives. It has financed innovation, built industries, connected economies and lifted hundreds of millions of people out of poverty. Few of us would seriously wish to reverse it.

Yet every system has consequences.

Perhaps the least discussed consequence of global capitalism is that it increasingly separates the place where wealth is created from the place where much of it is ultimately owned.

The two are no longer the same thing.

Britain Taught Me the Lesson Before Spain Did

Ironically, Britain had been teaching me this lesson for decades without my noticing.

Successive governments sold companies, utilities, railways, airports, property and infrastructure into private and often international ownership. We were told that this was modernisation, efficiency and the price of attracting investment. In many respects, it was.

Investment creates jobs.

Investment raises productivity.

Investment helps economies grow.

But every sale also carried another consequence.

A little more of tomorrow’s income would belong to someone else. And if the quality of a service such as buses and railways deteriorates in Manchester when the company owners sit in an office along the Champs Elysées, we should not be too surprised.

At the same time, Britain itself became a major owner of overseas assets. Pension funds, investment companies and multinational businesses accumulated wealth around the world. Perhaps that is one reason Britain has continued to generate considerable income despite producing far fewer of the manufactured goods that once defined its economy.

I had simply never connected those two facts before.

The newspaper in Spain finally joined the dots for me.

The Conversation We Rarely Have About Wealth

Political arguments usually revolve around wages, taxation or redistribution.

The left asks how wealth should be shared.

The right asks how more wealth can be created.

Both debates matter.

But perhaps they both overlook an earlier question.

Who owns the wealth before anyone starts arguing about how to redistribute it?

That seems to me to be one of the defining questions of our age.

Not because ownership should be concentrated within national borders.

Nor because global investment is somehow undesirable.

But because ownership itself has become strangely invisible.

Millions of people spend entire careers helping to create wealth while accumulating very little ownership of the economy they are helping to build.

They earn incomes.

But wages and ownership are not the same thing.

One pays today’s bills.

The other builds tomorrow’s security.

A Fairer Form of Globalisation

I have no desire to retreat into economic nationalism.

The extraordinary prosperity of the modern world owes much to capital flowing freely across borders. The challenge, surely, is not to make investment less global but ownership less exclusive.

Economic growth should not become a spectator sport in which millions of people spend their lives creating wealth they will never meaningfully own.

A healthy economy should produce not only better wages but broader ownership, because ownership is what allows one generation’s work to become the next generation’s security.

That does not require abandoning global markets.

It requires asking whether ordinary citizens have enough opportunities to become long-term owners of the prosperity they spend their lives creating.

What if governments devoted as much energy to widening ownership as they currently devote to encouraging growth?

What if employee share ownership became the norm rather than the exception?

What if ordinary citizens found it easier to build long-term stakes in productive businesses through pension funds, savings schemes and investment accounts?

What if the people whose daily work creates prosperity gradually came to own a larger share of that prosperity?

That strikes me as a far more constructive ambition than trying to turn back the clock on globalisation.

I still remember folding that newspaper and taking one last sip of coffee before walking home.

The headline had answered one question.

But it had raised another.

When we say that a country’s economy is booming, we usually ask how much wealth has been created.

Perhaps the more important question is one we almost never ask.

Who really owns the wealth that a nation’s workforce is creating?

“The political problem of mankind is to combine three things: economic efficiency, social justice and individual liberty.” — John Maynard Keynes

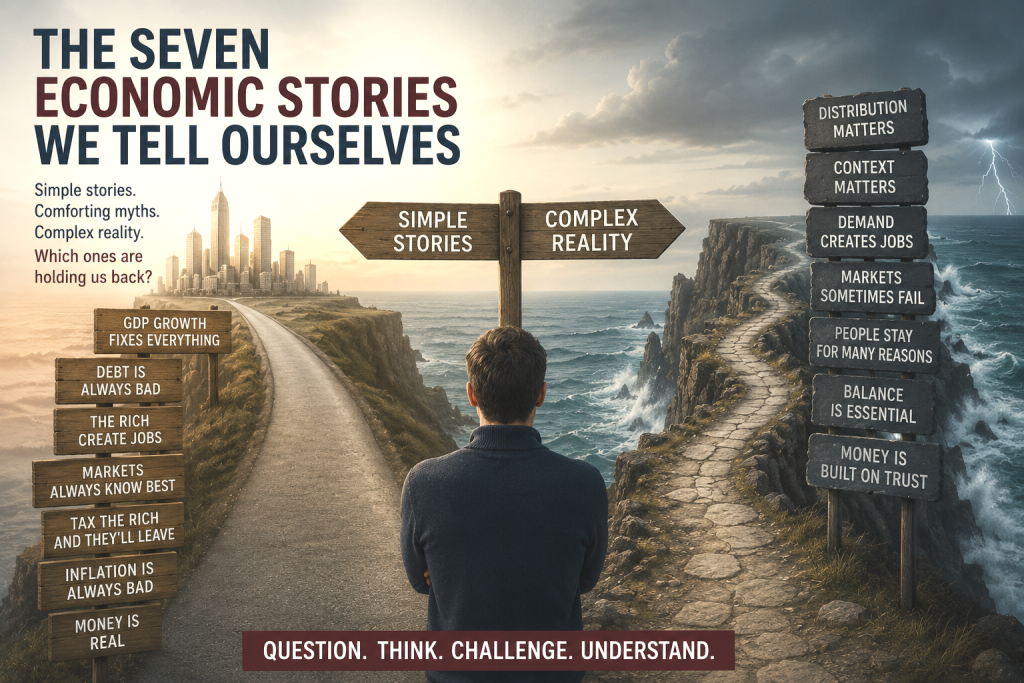

Last week I questioned whether our current school curriculum provides us with the knowledge we require for handling money during our adult life. This week I’d like to look at seven common economic myths I consequently grew up with that, I believe, should be examined by students in today’s education system.

Economics is often presented as a science of numbers. We hear about growth rates, inflation figures, government debt and stock market performance. Experts produce graphs. Politicians quote statistics. Journalists report percentages.

Yet much of our thinking about economics is not based on facts. We inherit economic beliefs in much the same way that we inherit religious beliefs, political loyalties, or assumptions about human nature. They become part of our mental furniture. We rarely examine them. We simply assume they are true.

Here are seven economic stories many of us have been taught to believe.

Myth No. 1. If GDP Is Growing, Everything Must Be Fine

One of the most common assumptions is that economic growth automatically means social progress. If the Gross Domestic Product is increasing, politicians congratulate themselves, commentators celebrate and newspapers announce that the economy is doing well.

But there is an obvious question that often goes unasked: doing well for whom?

GDP measures economic activity. It measures production. It tells us how much a country produces and sells. What it does not tell us is how that wealth is distributed or whether ordinary people are benefiting from it.

A nation can have impressive growth while housing becomes unaffordable, public services deteriorate and large sections of the population struggle to make ends meet.

As a former teacher, I sometimes compare GDP with examination results. A school may improve its statistics while becoming a worse place to learn. The numbers can look impressive while something essential is being lost.

The same is true of nations. Economic growth matters, but it is not the same thing as human flourishing.

Myth No. 2. Debt Is Always Bad

Most of us are taught to fear debt. For individuals, that is often sensible. Excessive borrowing can destroy lives. It can create stress, dependency and hardship. Yet not all debt is the same.

A mortgage, a student loan or a business investment is different from borrowing money to fund reckless consumption. One creates future value; the other merely brings tomorrow’s spending into today.

The same principle applies to governments. When a state borrows to invest in education, infrastructure, scientific research or healthcare, it may be creating assets that benefit future generations. The question is not whether debt exists, but whether the borrowing is productive and sustainable.

The most successful economies in the world often carry substantial public debt. What matters is not the existence of debt itself, but the wisdom with which it is used.

Myth No. 3. The Rich Create Jobs

This idea appears so frequently in political debate that many people accept it without question. There is, of course, some truth in it. Entrepreneurs create businesses. Businesses employ people. Investment can stimulate growth. But the story is incomplete.

Businesses do not hire employees simply because their owners are wealthy. They hire employees because there is demand for their products and services. A restaurant expands because customers fill its tables. A manufacturer recruits workers because orders are increasing. A shop hires staff because people are buying what it sells.

In other words, jobs are not created by wealth alone. They are created by economic activity. Moreover, much employment comes not from billionaires or multinational corporations, but from small and medium-sized businesses. Across Europe, countless family businesses, local shops, tradespeople and self-employed entrepreneurs collectively employ millions of people.

The real engine of employment is not wealth itself but a healthy and active economy.

Myth No. 4. Markets Always Know Best

For some people, the market has become almost a secular religion. The argument is familiar. Left alone, markets allocate resources efficiently. Government intervention merely creates distortions and stunts economic growth.

There is certainly some truth in this. Competitive markets can be remarkably effective. They often encourage innovation, efficiency and consumer choice. But markets are not infallible.

Consider healthcare. If access to medical treatment depends entirely upon ability to pay, many vulnerable people will be excluded.

Consider environmental protection. Businesses may profit by passing environmental costs onto society as a whole. Pollution becomes someone else’s problem.

Economists even have a term for these situations: market failures.

The reality is that markets and governments each have strengths and weaknesses. Mature societies require both. The challenge is not choosing one over the other, but finding the right balance between them.

Whenever someone insists that the answer is always more market or always more state, I become suspicious. Human societies are rarely that simple.

Myth No. 5. If You Tax the Rich, They Will Leave

This argument appears whenever tax reform is proposed. Raise taxes on wealthy individuals, we are told, and they will immediately pack their bags and move elsewhere.

At first glance, the claim seems plausible. Yet people are not spreadsheets.

Human beings make decisions based on family, friendships, culture, language, quality of life, security and belonging. Financial considerations matter, but they are rarely the only consideration.

Countries such as Norway, Sweden and Denmark have maintained relatively high levels of taxation while remaining prosperous, innovative and attractive places to live.

This does not mean taxes can be increased without limit. Excessive taxation can certainly discourage investment and entrepreneurship.

The point is simply that reality is more nuanced than political slogans suggest.

People stay for many reasons. They leave for many reasons. Tax is only one factor among many.

Myth No. 6. Inflation Is Always Bad

The word inflation usually arrives wrapped in anxiety. We hear that prices are rising and immediately assume disaster.

Certainly, high inflation can be deeply damaging. It erodes savings, creates uncertainty and hits those on lower incomes particularly hard. Yet economists generally do not aim for zero inflation.

A modest level of inflation is usually considered healthy because it reflects a growing economy. It encourages spending, investment and economic activity.

What is often forgotten is that the opposite problem can be equally dangerous.

If prices continually fall, people postpone purchases. Why buy today if everything will be cheaper tomorrow? Businesses then sell less, investment slows and unemployment may rise.

Like many things in life, the issue is not inflation versus no inflation. It is balance. Too much inflation can be destructive. Too little can be equally problematic.

Myth No. 7. Money Is Real

This final myth is my favourite because it takes us beyond economics and into philosophy.

Most of us think of money as something solid and tangible. We earn it, spend it, save it and worry about it. Yet money possesses no intrinsic value.

A fifty-euro note is merely paper. The number displayed in your bank account is simply a digital record stored on a computer somewhere.

Money works because we collectively believe it works. Its value depends upon trust.

This is not as strange as it sounds. Much of human civilisation rests upon shared beliefs. Nations exist because enough people believe they exist. Laws function because people collectively accept their legitimacy. Companies, universities and governments all depend upon systems of shared trust.

Money is one of humanity’s most successful collective stories. That does not make it imaginary. It makes it a social construct, like any other.

And perhaps that is one of the most important lessons economics can teach us.

If only I’d known in my twenties what I know now

If there is a lesson I wish somebody had taught me when I was starting out, it is that wealth is rarely built through cleverness alone. Looking back, the people who seem to achieve financial security are often not the most intelligent, the most educated or even the highest earners.

They are the people who consistently do a few simple things well.

They spend less than they earn

They avoid unnecessary debt

They acquire productive assets

They diversify their investment portfolio

They think long term

And above all, they allow time and compounding to work their quiet magic.

Perhaps that is the greatest economic lesson of all. Not that there are easy answers. But that small, sensible decisions repeated over decades are often more powerful than brilliant ideas pursued for a few months.

Beyond Economics

The purpose of examining these myths is not to replace one certainty with another.

It is to become more cautious whenever someone offers a simple explanation for a complicated problem.

Economic debates are often presented as battles between truth and error, between common sense and foolishness, between left and right. Reality is usually less satisfying.

The older I become, the less interested I am in certainty and the more interested I am in questions.

Who benefits from economic growth?

What kind of debt creates value?

When do markets work well, and when do they fail?

How much inequality can a society tolerate before trust begins to erode?

And perhaps most intriguingly of all: what other things do we collectively believe in that are no less dependent on faith than money itself?

Economics turns out to be about far more than money.

It is about human beings and the stories we tell ourselves about how society works.

The test of a first-rate intelligence is the ability to hold two opposed ideas in mind at the same time and still retain the ability to function.

The British government has this week announced plans to ban social media access for under-16s. Ministers describe it as a historic intervention to protect children. Newspapers are full of discussion about algorithms, screen addiction and online harms. Yet as I watched the announcement unfold, I found myself asking a different question entirely. Why are we once again arguing about what children should be prevented from doing rather than what they should be taught?

The discussion is presented as a matter of national importance. Ministers speak gravely about online harms. Newspapers speculate about restrictions and enforcement. Experts are summoned to television studios. Committees are established. Reports are commissioned.

But all of my experience as a student and teacher tells me that we are arguing passionately about the wrong problem. At sixty-five years of age, having attended good schools, won a scholarship to Oxford, taught for decades and worked in several countries, I have reached an uncomfortable conclusion: almost nobody ever taught me how money works.

Nobody explained investing. Nobody explained compound interest. Nobody explained pensions. Nobody explained the long-term consequences of inflation. Nobody explained the relationship between taxation and public services. Nobody explained mortgages beyond the most superficial level. Nobody explained the astonishing difference between acquiring assets and merely consuming income.

Yet these are not specialist concerns. They are among the most important forces shaping the lives of ordinary citizens.

They influence where people live, when they retire, whether they accumulate wealth, how vulnerable they are to economic shocks and, ultimately, the degree of freedom they enjoy throughout their lives.

The strange thing is that this educational failure is almost invisible. Some parents complain if their children leave school unable to read Shakespeare. Politicians worry if socially constructed examination results fall.

Universities debate decolonisation, inclusion, safe spaces and artificial intelligence.

Meanwhile, millions of young adults enter the world with little understanding of debt, investment, taxation, pensions or wealth creation.

Nobody seems particularly alarmed. But as a teacher, I find this extraordinary. And as a citizen, I find it deeply disturbing.

As someone who grew up in a working-class family, I find it difficult to avoid an even more uncomfortable observation.

Those who grow up in affluent families often learn these things anyway.

They hear conversations around the dinner table. They observe parents discussing property, investments, inheritance and taxation. They absorb financial knowledge almost by osmosis.

Those from less privileged backgrounds are often far less fortunate.

The result is that schools, which are supposed to reduce inequality of opportunity, usually end up reinforcing it.

I studied languages, theology, literature and philosophy. I do not regret a moment of it. Education transformed my life and broadened my horizons in ways I shall always be grateful for.

Yet if I am completely honest, my grandfather, a builder with far less formal education, may well have understood practical wealth creation better than I did. He understood property. He understood value. He understood patience. Most importantly, he understood that money is not primarily about income. It is about what income becomes over time. That lesson alone may be worth more than half the curriculum I studied. Unfortunately, he passed away when I was five years old, so he could never pass on his wisdom.

The question therefore is not whether children should be protected from harmful content online. Of course they should.

The question is why governments find it easier to regulate TikTok than to ask whether the curriculum itself is preparing young people for adult life.

Why is there endless discussion about screen time but comparatively little discussion about economic literacy?

Why do we devote thousands of classroom hours to subjects that many pupils will never use again while allocating almost no serious time to understanding mortgages, pensions, inflation, taxation, investing and economic reasoning?

And why, after decades of educational reform, do so many intelligent, capable and highly educated adults still feel financially illiterate?

These are not merely personal questions. They are political questions. They are social questions.

And they are ultimately questions about power.

A population that cannot critically evaluate economic arguments is easier to persuade, easier to frighten and easier to divide. It becomes dependent upon experts, commentators and politicians to interpret reality on its behalf.

A population that understands economics is harder to manipulate.

Perhaps that is why the seven economic myths I recently encountered fascinated me so much. I will share them here next week.

These seven myths didn’t just reveal something about economics, but they revealed something about education.

And perhaps, more importantly, about what education still fails to teach.

“Education is not the filling of a pail, but the lighting of a fire.”

— W. B. Yeats

If Yeats was right, then perhaps we need to ask whether we are lighting the wrong fires.

Recently, Gregor Gysi made an observation that deserves far more attention than it has received. According to Gysi, Friedrich Merz’s political strategy is increasingly based on finding new groups of people to blame for Germany’s socio-economic problems rather than confronting the deeper causes of the country’s decline.

First it was immigrants and refugees.

Then it was the healthcare system.

Now it is Germany’s workforce.

Whether one agrees with Gregor Gysi on everything or not, his criticism exposes a troubling pattern. Whenever Germany faces a serious challenge, Merz appears more interested in identifying a convenient target than offering either a compelling vision for the future or consistent decisions aligned with clear political and ethical values.

The Refugees Who Helped Germany

Germany welcomed around one million refugees during the migration crisis of 2015 and 2016. The decision was controversial then and remains controversial today, stoked up by the nationalism of the AfD.

Yet ten years later, many of these refugees have integrated successfully. They have learned German, entered the labour market, started businesses, paid taxes, contributed to the pension system and become part of German society.

Some arrived as highly qualified professionals: doctors, engineers, academics and lawyers. Others filled essential jobs that Germany struggles to recruit for itself.

Germany’s demographic crisis is not a future problem. It is happening now. Employers across the country face labour shortages. The pension system depends on a shrinking workforce supporting a growing retired population.

I recently thought of a young Syrian woman I know. She now speaks fluent German, as well as English and Arabic. She is completing a doctorate in law and has every prospect of becoming a highly productive member of German society.

Yet she is planning her future elsewhere, most likely in the United States.

Germany invested in her integration. Germany benefited from her talent. Germany may now lose her altogether.

That is not a success story. It is a failure of political imagination.

Scapegoating Healthcare

The same pattern appears in healthcare.

Germany undoubtedly faces major financial pressures in its health and social insurance systems. An ageing population, rising costs and economic stagnation create genuine challenges.

But the answer cannot simply be to reduce protections that millions of people rely upon.

The principle that families should have access to healthcare regardless of income has long been one of the strengths of the German social model. Weakening that principle may save money in the short term, but it risks creating greater social and economic costs in the future.

What is particularly striking is the contrast between the urgency applied to military spending and the hesitation shown towards investments in social infrastructure.

Politicians readily describe defence spending as an investment in the future. Yet healthcare, education and social stability are investments too.

A nation is not defended only by weapons. It is defended by healthy, educated and confident citizens.

The Myth of Working Longer

The latest target appears to be Germany’s workforce.

Merz has argued that Germans need to work more hours and remain economically active for longer. On the surface, this sounds practical and responsible.

Productivity depends upon motivation, trust, leadership, skills, technology and working conditions. A well-managed and valued employee working thirty-five hours per week can often contribute more than an exhausted and disengaged employee working fifty-five.

The most successful economies do not necessarily have the longest working weeks. They have the most productive working hours.

Germany’s challenge is not primarily that its people are lazy. It is that investment in digitalisation, reducing bureaucracy, promoting infrastructure and innovation has lagged behind many competitors for years.

Blaming workers is easier than fixing structural problems. But it is also less effective.

Germany Needs Leadership, Not Scapegoats

Friedrich Merz undoubtedly possesses ambition. He looks like a statesman. He speaks confidently. He projects authority.

Yet genuine leadership requires more than authority.

It requires empathy.

It requires vision.

It requires values.

The CDU once prided itself on balancing economic responsibility with social responsibility. Today, that balance often seems absent. The willingness to embrace large-scale borrowing while simultaneously questioning social protections creates the impression not of strategic thinking but of political inconsistency.

Germany faces enormous challenges: demographic decline, economic stagnation, digital backwardness, labour shortages and growing political polarisation.

None of these problems will be solved by blaming refugees, healthcare recipients or workers.

They require something much rarer.

They require a government willing to unite rather than divide.

For all his political flaws, Gregor Gysi has long understood one simple truth: a society becomes stronger when it expands the circle of belonging rather than narrowing it. He truly is the best chancellor Germany never had.

Germany’s future will depend on whether more of its leaders understand that truth as well.

“When five people own more wealth than the poorer half of an entire nation, the problem is not refugees, nurses or workers. The problem is where the wealth has gone.” — Gregor Gysi (paraphrased from his speeches on wealth inequality)

A newspaper headline over breakfast in Spain made me question something I’d never really considered before. When a country’s economy is booming, who actually owns the wealth that’s being created?

A newspaper headline over breakfast in Spain made me question something I’d never really considered before. When a country’s economy is booming, who actually owns the wealth that’s being created?

The British government has this week announced plans to ban social media access for under-16s. Ministers describe it as a historic intervention to protect children. Newspapers are full of discussion about algorithms, screen addiction and online harms. Yet as I watched the announcement unfold, I found myself asking a different question entirely. Why are we once again arguing about what children